Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

President Christine Lagarde had barely begun unveiling the European Central Bank’s new monetary policy strategy this month when she signaled that the Germans were on board.

By quickly highlighting officials’ unanimous backing, she revealed the support of Bundesbank chief Jens Weidmann -- validation that also underscored how the hawkish and conservative institution he leads is committed to exerting influence through engagement rather than confrontation, and is quietly satisfied with the results.

Inflation Trend

Price growth has been persistently below 2% and ECB goal for years

Source: Eurostat, Bloomberg calculations

Compare that to the history of Bundesbankers’ temper tantrums against ECB policies over the years, featuring bitter resignations and disagreements fought out in court, capped by outcomes that often defied their wishes anyway. If anything, the review’s outcome emphasizes a very different rapport than used to be the case.

“There’s a certain pacification in the relationship, a better cooperation, and an acknowledgment that you have to get along,” said Guntram Wolff, director of the Bruegel think tank in Brussels. “There’s a fine line between being hawkish, which is a justified position, and being perceived as anti-euro.”

Lagarde’s accession to the ECB presidency and a different style to her predecessor, Mario Draghi, were important in resetting the Bundesbank relationship. And with elections in September in Germany, Europe’s biggest economy, she recognizes the need to sustain its support for the euro amid skepticism about policies such as negative interest rates.

An initial trial of the new monetary strategy, and the consensus underpinning it, will take place this week, as the Governing Council meets for a decision on Thursday that will result in revamped guidance on its future policy.

New Strategy

The approach Lagarde unveiled on July 8 included a new higher inflation target of 2% and discretion for officials in bolstering growth. That outcome reflected a compromise Weidmann was closely involved in wording as concrete drafts for the revamp circulated after a retreat of policy makers northeast of Frankfurt.

The language acknowledges an overshoot of the goal can happen when interest rates are very low, but stops short of making it an actual aim. By contrast, the Federal Reserve’s strategy unveiled last year does that by adopting average inflation targeting.

“We are not striving for either lower or higher rates,” Weidmann said after Lagarde’s announcement. “That was important to me.”

The Bundesbank also steered climate-change policy toward managing balance-sheet risks, instead of more radical options that its officials felt were better handled by governments.

The result is a monetary strategy that observers see tilted in a more dovish direction but that still accommodates the sensitivities of an institution with a special role in Europe’s monetary union, with its tight-money regime providing the blueprint for the ECB at its foundation in 1998.

“I’m glad to see that the ECB withstood the temptation to throw its entire strategy overboard,” Otmar Issing, the former Bundesbanker who served as the ECB’s first chief economist and who helped design its original policy framework, said in an interview. “Changing the inflation goal to a straight 2% was the right choice and long overdue. Highlighting the medium-term focus is important.”

By contrast, Juergen Stark, the former Bundesbank vice president who succeeded Issing in 2006, is more critical.

“I have considerable doubts that the new price-stability goal will create more clarity if the central bank insists on greater flexibility,” he said. “Clarity and flexibility are at odds with each other, and in the worst case it hurts credibility.”

Such sentiments provide not only a glimpse of the Bundesbank’s misgivings over the years, but also hint at the difficulties Lagarde might have faced if the Germans hadn’t played ball.

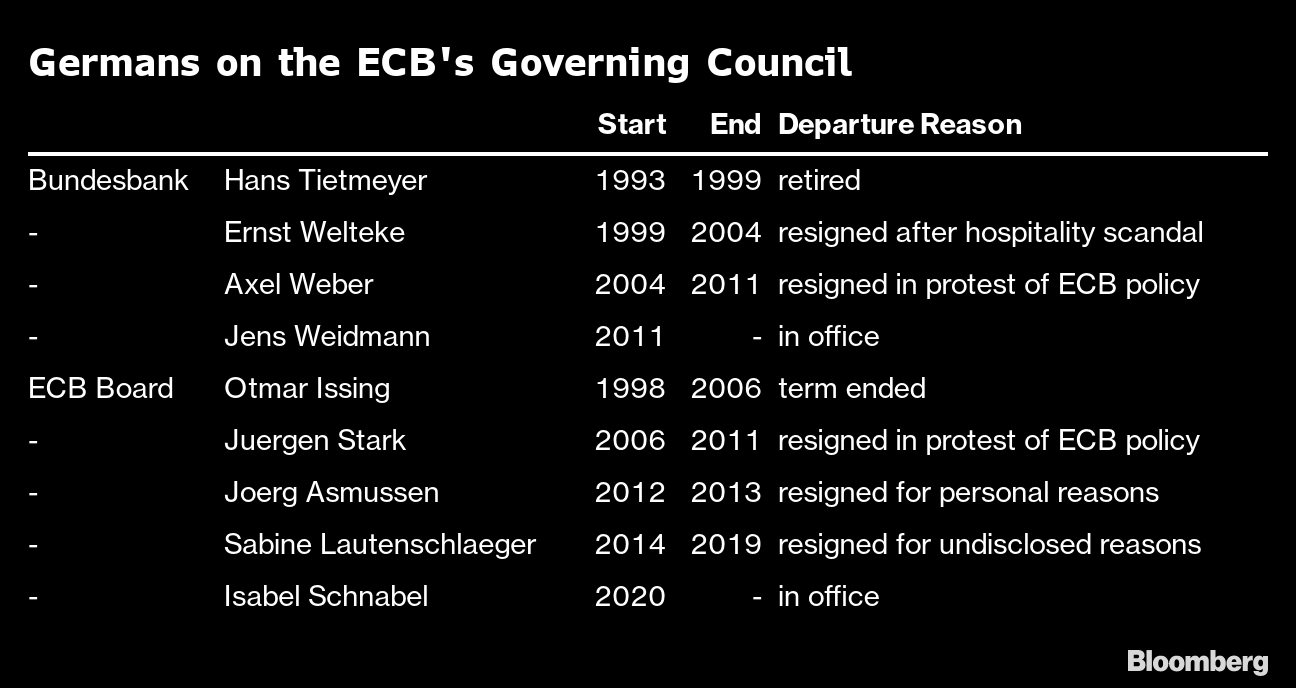

Notable instances of past acrimony include arguments over the ECB’s first sovereign bond-buying program preceding the 2011 resignations of both Axel Weber, Weidmann’s predecessor as Bundesbank chief, and of Stark too.

Germans on the ECB's Governing Council

Weidmann himself said that quitting “wouldn’t be my style,” but he instead became a thorn in the side of Draghi, who accused the German of saying “no to everything.”

The Bundesbanker even testified in court against his colleague’s famous “whatever it takes” policy to stem the region’s sovereign debt crisis, and also claimed that his own central bank isn’t just one of many in the euro zone -- but the “largest and most important” of them.

Such confrontations fed a stereotype of the Bundesbank as an orthodox behemoth that overlooked moments of pragmatism. Its officials often took a flexible approach to managing money supply and inflation for example, and dabbled in quantitative easing in the 1970s. Even after Weidmann opposed Draghi’s use of the policy in 2015, he engaged in dialog over its execution.

Lagarde knows that consensus over strategy doesn’t guarantee support on its implementation. She told the Financial Times last week that she’s under no illusion that decisions will be unanimous.

It also remains to be seen if the Bundesbank’s pragmatism ultimately reflects a moderation in its hawkishness, or simply a more diplomatic demeanor.

“As long as the ECB continues to expect too-low inflation, the new strategy would require it -- strictly speaking -- to loosen its policy,” said Christian Odendahl, chief economist at the Centre for European Reform in Berlin. “The true test of the negotiated consensus is still ahead.”

"strategy" - Google News

July 19, 2021 at 11:00AM

https://ift.tt/3wOGGJw

Lagarde's Strategy Hints at New Era of ECB Teamwork With Germans - Bloomberg

"strategy" - Google News

https://ift.tt/2Ys7QbK

https://ift.tt/2zRd1Yo

Bagikan Berita Ini

0 Response to "Lagarde's Strategy Hints at New Era of ECB Teamwork With Germans - Bloomberg"

Post a Comment