Oil and gas producers seemingly have settled on a strategy. OPEC and Russia will limit production and let prices rise during a global war-famine-pandemic. OPEC sets the price umbrella while the Russians discount the price for obvious geopolitical reasons. All other big oil producers adhere to pricing and supply discipline knowing that OPEC’s costs of production are so low that OPEC can undercut any oil producer that ignores pricing discipline. The big US producers say they will not expend capital to increase supply when they lack assurance of continued demand. As for high prices, they result from competition in the market, the oil CEOs say. We all know how this will end, as it always does: demand will weaken and producers who would rather get a lower price than let some other producer get the business will cheat. But not for a while.

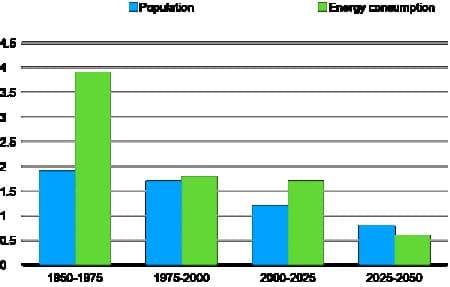

What about energy demand over the long term? Most forecasters predict global demand through 2050 will grow at around 1% a year or less. Some get their numbers from econometric models, others from a painstaking analysis of end-use demand. We suggest a simple way to check out those projections using another projection likely to be reasonably accurate, namely population growth. Figure 1 compares rates of growth for world population and world energy usage. (Actual numbers for 1950, 1975, and 2000, and estimates for 2025 and 2050 (from standard sources)).

Figure 1. Annual rates of growth (%).

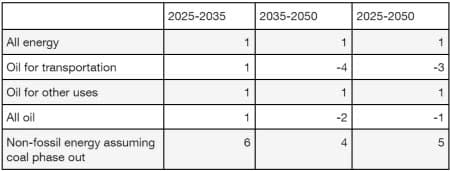

After OPEC’s assault on the international order in the 1970s, which dramatically raised oil prices, growth in energy consumption slackened. Consumers learned to use less. Might that happen again? Projections put energy demand growth a bit under population growth. So let’s make a few conservative assumptions. In the past, energy usage grew faster than population. So, let’s use 1% per year as a minimum number for energy demand growth. Now to oil. Demand, under normal circumstances, ought to grow in line with all energy. Transportation accounts for roughly 60% of oil consumption, and the number of cars on the road grows by roughly 1% per year. But sometime around 2035 automobile producers will stop making vehicles with internal combustion engines. From that point forward, petroleum sales to transportation will fall, maybe by 4% per year, as consumers retire old cars and replace them with electric vehicles. Assuming that non-transportation oil usage continues to grow by 1% per year, overall oil consumption in 2050 would fall 14% from 2025 levels. Green energy resources, to fill the gap, would have to grow several times faster than demand for energy as a whole, especially if coal is phased out of use as a boiler fuel. Table 1 shows the growth rates:

Table 1. Annual growth rates for energy consumption (%)

If you are an executive or director in the oil business, you already know the picture, but you want to extract as much cash out as you can before the direction of demand becomes clearer. You don’t want to scare investors (because you have a big stake in stock options). You want to encourage employees present and future. And you need to impress on politicians that the gloomy future of the business is due to unreasonably impatient climate activists and the government has to help. But that is all for the corporate communications people to hash out. What do you do with all the cash pouring in because oil prices are high and you have kept the drilling budget low because you don’t expect drilling to earn a return commensurate with risk?

Oil companies flush with cash could invest in another business, such as renewables, as European energy companies have done. Or they can return excess cash to shareholders as dividends or stock buybacks but this is an admission that future investment prospects in oil are poor. Paying higher dividends has three drawbacks. First, a higher dividend triggers higher income taxes for the stockholders at the normal tax rate. Second, it might take too long to pay out the money. Third, setting the corporate dividend policy at a higher level creates expectations that the company will pay higher dividends in the future, as well, and this is clearly not the expectation the company wants to create.

As an alternative, companies can use cash to repurchase stock. By doing so they boost the stock price so shareholders get a better price if they sell, and lower the number of shares outstanding, thereby raising earnings per share. Those who sell their stock at a profit only pay a capital gains tax, which is usually lower than the tax rate on dividend income. Unlike changes in dividend policy, companies can execute share buybacks quickly and flexibly, a plus. Executives whose bonus and stock options are based on earnings per share and stock price can earn more, too. That may tilt the decision to share buybacks rather than increased dividends.

What messages do share buybacks send? First, corporations buy back shares when they can’t come up with something better to do with excess cash flow. That says a lot about senior management’s view of the prospects for their business. Second, oil companies could face big-time litigation. Remember that Texas law that empowered anyone to sue anyone connected to an abortion? Or the California law that allowed anyone to sue any person who sold an assault rifle? Well, NY politicians are thinking about a law to allow anyone to sue those causing climate damage. And, no doubt some will accuse fossil fuel companies and users of misleading investors about climate change. More lawsuits? Moving the money out of the business makes the oil company a less enticing target for a mammoth lawsuit. Again, not an encouraging message.

So, what’s an appropriate strategy for oil company executives given the uncertainties we’ve discussed? From a short-term business perspective, oil companies should aggressively return cash to shareholders, refrain from new investment, and, if they have enough politicians still beholden to them, stall climate mitigation as long as possible while reaping the reward of high prices. And stave off calls for any excess profits taxes. But what about the long term, the impact of high prices on demand, and the reputational damage done by enjoying high profits during a period of distress, famine, and war? We would conclude, from the unwillingness to invest and the stock buybacks that oil company managers themselves have lost faith in the future of oil. So, if you don’t see much of a future in your business, and nobody stands in your way, and it’s legal, you might as well maximize what you can collect now. As John Heywood put it, back in 1546, “When the sun shineth, make hay.” That’s capitalism, isn’t it?

By Leonard S. Hyman and William I. Tilles

More Top Reads from Oilprice.com:

Read this article on OilPrice.com

"strategy" - Google News

January 01, 2023 at 05:00AM

https://ift.tt/x2ft1wZ

The Right Strategy For Oil Companies In 2023 - Yahoo Finance

"strategy" - Google News

https://ift.tt/2NaCSPt

https://ift.tt/qQyPIBD

Bagikan Berita Ini

0 Response to "The Right Strategy For Oil Companies In 2023 - Yahoo Finance"

Post a Comment