getty

These days, I’m hearing from a lot of folks who are pretty nervous, bracing for yet another round of dividend cuts to hit them out of the blue.

It’s understandable. Recently, we’ve seen plenty of dividend “sacred cows,” like Wells Fargo (WFC), mall landlord Simon Property Group (SPG), and senior-care operators Welltower (WELL) and Ventas (VTR) cut or eliminate their payouts.

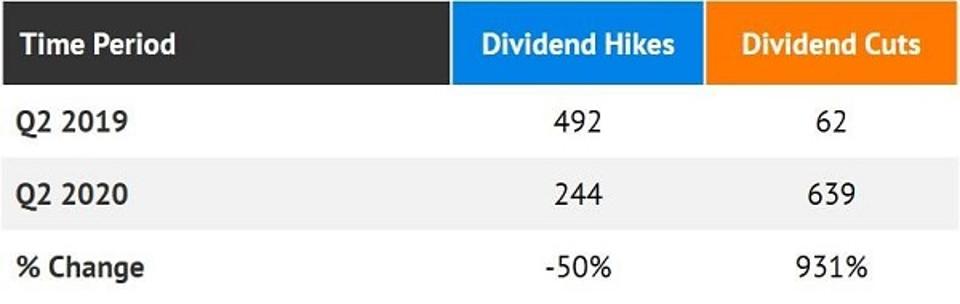

In the second-quarter of 2020, 244 firms increased their dividends, according to Howard Silverblatt of S&P Dow Jones Indices. That sounds good until we see that 639 companies decreased their payouts. In other words, dividend investors were two-and-a-half times as likely to receive a pay cut as they were a raise. Yikes.

Contrarian Outlook

At this rate we’re going to hear income investors asking for government assistance!

Dividend cuts, of course, not only crush your income but take a chunk out of your nest egg as investors dump the stock in response. This is what happened to Welltower shareholders, who took a double hit as their plummeting dividend took the share price down with it.

The good news is that (hard as it is to believe) there are signs of stability on the dividend front. They come from investment firm Janus Henderson, former home of our old friend, the Bond King, Bill Gross.

Janus tells us that spending on dividends plunged $108 billion, or 22%, worldwide in the second quarter. But here’s the twist: essentially all of this 22% drop came from outside the US. American companies’ spending on dividend payouts was basically flat in Q2, falling an imperceptible 0.1%.

I know what you’re thinking: how can that be, when Silverblatt tells us the number of cuts far outweighed the number of hikes in the US in Q2? It’s mainly because Janus tracks just 335 US companies for its index (296 of which maintained or hiked their payouts), compared to the much wider universe Silverblatt uses.

Nonetheless, it does suggest US dividends are more resilient than those in other countries. You can see this strength in a company with “America” right in its name: American Tower (AMT).

You may know of AMT; it rents out its cell towers to US telecom firms like AT&T (T), Verizon (VZ) and T-Mobile US (TMUS). It’s kept its dividend popping higher for years—right through the pandemic—bringing its share price along for the ride!

But of course, not all US dividends will be safe as we move into the fall, when we could face a resurgence of the virus and a (possibly disputed) presidential election.

So how do we protect ourselves from surprise payout cuts?

I’ve got you covered there, too. Let’s run through two simple strategies—and two specific tickers worthy of your attention today.

Step 1: Be a Dividend-Growth Hawk

The fact is, there were hints Welltower’s dividend wouldn’t hold up in a recession. The most obvious was a slowing (and eventual stalling out) of its dividend growth.

We got our first sign that Welltower was slowing in May 2017, when management announced a token one-cent increase, less than the (still meager) three-cent hikes it had been rolling out. That was the proverbial canary in the coalmine.

Then came the big “tell”: management left the payout untouched for three years.

So what’s our takeaway here?

I’d suggest viewing all your stocks through a lens like this. If any have a record of dividend growth that downshifts (or stalls out completely), you’ll want to dig deeper and see what’s really going on. I’ll show you my most reliable dividend-safety indicator below.

But this isn’t just about heading off dividend cuts—you can use the same approach to set yourself up for rising dividends and share prices by focusing on stocks whose dividends are growing fast, and ideally accelerating. American Tower, which typically hikes its payout every quarter, is one example. But it’s not the only one.

Another is Mastercard (MA), which doesn’t get any income-seeker’s blood pumping with its 0.5% current yield. But that headline number masks its breathtaking payout growth: in the last decade, Mastercard has hiked its dividend 2,500%. As with American Tower, investors have taken note and driven up the share price in response, to the tune of 1,600% in Mastercard’s case.

And Mastercard’s dividend is indeed accelerating.

That’s the exact opposite of the chart we saw with Welltower!

Mastercard is never cheap, usually trading around 30X to 40X forward earnings. But the company’s massive electronic-payments network makes it a key player in the pandemic-driven shift away from cash. That will let it keep rolling out big dividend hikes—no matter what happens this fall, in 2021, or beyond.

Right now, the company pays 22% of free cash flow (FCF) as dividends, so it could double its payout tomorrow and still be well below the 50% of FCF I consider safe. Dividends don’t get more reliable than that—which is why this stock is a good candidate to buy and tuck away for the next decade (or more).

Step 2: Demand a Low Payout Ratio

We’ve talked a lot about dividend growers so far, but what about the portion of your portfolio you devote to current income? That would include stocks that don’t grow their payouts as much over time, instead rewarding you with higher yields now.

For these stocks, the payout ratio, which we touched on above with Mastercard, is critical. With regular stocks, I prefer to use the last 12 months of dividends divided by the last 12 months of FCF.

That’s different from how most investors calculate the payout ratio; they prefer to use net income. But FCF, or the amount of operating cash flow left over after capital expenses, is more accurate. Think of it as a snapshot of how much money a company has on hand to repay debt, buy back shares or pay dividends at a given time.

Real estate investment trusts (REITs) like Welltower are different because they’re pass-through investments: they take enough of the rent they collect to fund their operations, then pass the rest on to you. As such, they can boast sustainable payout ratios of 80% to 90%.

But for maximum safety, I prefer REITs with lower ratios, like apartment landlord Equity Residential (EQR). It’s paid out just 65% of FFO as dividends over the last 12 months, offers an attractive 4.3% yield and boasts strong payout growth, with the dividend up 20% in the last three years!

Even so, the mainstream crowd is down on the stock (EQR is off 32% this year). But that pessimism seems unlikely to last: the US unemployment rate is falling as the economy reopens; EQR collected 97% of its rental income in Q2; and it held a 95% occupancy rate.

EQR’s depressed share price leaves it with a dividend yield higher than it’s been since 2009 and trading at a bargain 15-times FFO, to boot.

Brett Owens is chief investment strategist for Contrarian Outlook. For more great income ideas, get your free copy his latest special report: Your Early Retirement Portfolio: 7% Dividends Every Month Forever.

Disclosure: none

"strategy" - Google News

September 02, 2020 at 07:50PM

https://ift.tt/3hV8XHF

My No. 1 Strategy For Dodging Dividend Cuts - Forbes

"strategy" - Google News

https://ift.tt/2Ys7QbK

https://ift.tt/2zRd1Yo

Bagikan Berita Ini

0 Response to "My No. 1 Strategy For Dodging Dividend Cuts - Forbes"

Post a Comment